When my main credit card got yanked for some kind of fraud activity earlier this month (as it seems all of them do, sooner or later) I had the unpleasant task of going back over my bills to see what companies I’d need to give a new credit card number. Among those many (Amazon, Apple, PayPal, Dish Network, EasyPass…) were a bunch of magazines that get renewed annually. These include:

My wife, who is more mindful of money and scams than I am, urged me to stop subscribing automatically to all of them, because all their rates are lowest only for new subscribers. So I looked back through my last year’s bills to see what I was paying for each, and then at what they pitched new subscribers directly, or though Amazon.

Only Consumer Reports‘ price appears (at least in my case) to be lower for existing subscribers than for new ones. All the rest offer their lowest prices only to new subscribers.

Take The New Yorker for example. It’s my favorite weekly: one to which I have been subscribing for most of my adult life. Here’s my last automatic payment, from July of last year:

Now here is the current lowest price on the New Yorker website:

That doesn’t give me the price for a year. So I hit the chat button and got an agent named Blaise B. Here is what followed:

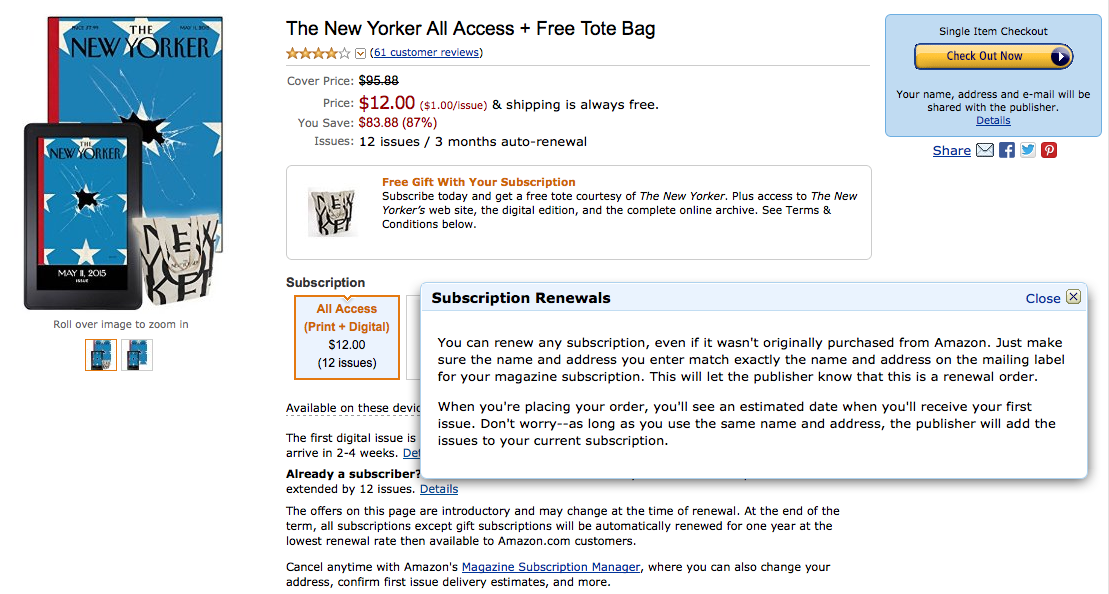

Meanwhile, here is the New Yorker deal on Amazon:

It’s the same $12 for 12 weeks, with no mention of cost after that. Nor is there any mention of the true renewal price.

It’s the same $12 for 12 weeks, with no mention of cost after that. Nor is there any mention of the true renewal price.

How is this not about screwing loyal subscribers? That it’s pro forma for most magazines? No. It’s just wrong — especially for a magazine with subscribers as loyal as The New Yorker‘s.

So I won’t be renewing any of those magazines, other than Consumer Reports. I’ll let them lapse and then re-subscribe, if I feel like it, as a new subscriber.

Meanwhile I will continue to urge solving this the only way it can be solved across the board: from the customer’s side. I explained this three years ago, here.

Leave a Reply