follow-up (June 19, 2010): See today’s New York Times article, “Peddling Relief, Industry Puts Debtors in a Deeper Hole” (reg. needed)

![]() Our mention last month of an upcoming FTC Debt Settlement Workshop attracted some “comment spam” from NetDebt, a for-profit company that “negotiates” with creditors in an attempt to reduce your overall debt. NetDebt calls itself a “100% online debt settlement solution” and emphasizes the participation of lawyers in providing its services (nonetheless, you apparently never meet your lawyers). They claim that “In some cases, your total debt will be cut in half.”

Our mention last month of an upcoming FTC Debt Settlement Workshop attracted some “comment spam” from NetDebt, a for-profit company that “negotiates” with creditors in an attempt to reduce your overall debt. NetDebt calls itself a “100% online debt settlement solution” and emphasizes the participation of lawyers in providing its services (nonetheless, you apparently never meet your lawyers). They claim that “In some cases, your total debt will be cut in half.”

I first heard of NetDebt on June 9th, when they tried to plant a link from f/k/a to their affiliated weblog, in order to increase NetDebt’s online profile. When the Comment showed up for “moderation,” my response was: “I just looked at your ‘NetDebt’ web site and have many questions about your services — especially the fees. Until I get a chance to review it more fully, I do not want a link from this weblog to yours, and have removed your URL.”

Having now looked more deeply into NetDebt, I want to present my continuing concerns about their fees — which are 15% of the amount of debt you bring to their program (regardless of results or the number of creditors it must deal with), plus a “small” monthly service fee of $50.

For example, the so-called “flat” 15 % fee would be $1500 if you have $10,000 of debt in the program; $3000 for $20,000 of debt; $6000 in fees for a $40,000 debt load. The $50 monthly service fee quickly adds up, too, and would add another $2700, if you stay in their program the full 54 months.)

Although many debt negotiators make no mention of the cost of their services at their websites, it appears that similar percentage-based fees have become common among debt settlement firms. (See, for example here and there) update (July 25, 2008): As discussed below, in response to this posting, Charles Phelan has written an extensive”History of Debt Settlement Fees” at The ZipDebt Blog (July 25, 2008).

Despite the traditional lawyer reluctance to talk about excessive fees, I hope that legal ethics counsel or professors, other lawyers, and consumer advocates will help us determine if or when such fees are “reasonable” or appropriate for lawyers to charge. At a time when many in the legal profession are promoting the use of “alternative” and “value-based” fees instead of hourly billing — while offering so little guidance on how to make the switch in an ethically-responsible manner — it would be especially useful to hear what standards or criteria they believe should be applied to prevent excessive fees under our professional and fiduciary principles. My assumption is that “what the market may bear” is not an appropriate test for protecting consumers — especially unsophisticated ones in dire economic straits — from unreasonably high legal fees. [Consumers can get some tips for protecting themselves in our post “understanding and reducing attorney fees“.]

There are many voices on the internet warning about “debt settlement scams” and the money wasted due to the high fees. [For example, this post at the ZipDebt Blog, and this article.] An article from SmartMoney.com, “Debt Settlement Could Cost More Than You Think” (June 20, 2007), gives an excellent summary. SmartMoney says, “Debt settlement is, in fact, a perfectly legal solution for consumers who are in deep and seeking an alternative to bankruptcy. But having a debt-settlement company do the legwork for you is fraught with risk, not to mention outrageous fees.”

Still, unless the purveyors are engaged in actual fraud or deception, regulators can’t do much about non-lawyers charging excessive fees for a questionable service that exploits desperate people, beyond providing information and warnings. However, the legal profession can hold lawyers to a higher standard and should require lawyers engaged in debt settlement to charge only reasonable fees. As with many similar easy-money schemes, my guess is that the services would not be offered by members of the Bar, if only a fair price could be charged.

Background: The f/k/a Gang has been skeptical for over a decade about the value of “debt reduction” services: Although there may be exceptions, in general, they appear to be overpriced, to be marketed with unrealistic claims, to use questionable tactics in gaining negotiation leverage (i.e., telling clients to stop making all payments to creditors), and to downplay the harm their tactics can cause to the credit rating of many of their clients. In addition, I believe that a significant number of consumers with large credit card debt are fully capable of “negotiating” directly with their creditors (that is, writing or calling to explain their financial situation and haggle for a reduction in the total debt owed), instead of using a debt settlement firm.

Background: The f/k/a Gang has been skeptical for over a decade about the value of “debt reduction” services: Although there may be exceptions, in general, they appear to be overpriced, to be marketed with unrealistic claims, to use questionable tactics in gaining negotiation leverage (i.e., telling clients to stop making all payments to creditors), and to downplay the harm their tactics can cause to the credit rating of many of their clients. In addition, I believe that a significant number of consumers with large credit card debt are fully capable of “negotiating” directly with their creditors (that is, writing or calling to explain their financial situation and haggle for a reduction in the total debt owed), instead of using a debt settlement firm.

As TrueCredit.com (sponsored by the credit bureau TransUnion) notes: “Everything that an agency can do, you have the power to do on your own. You can reduce your debts, negotiate settlements and improve your credit score from the comfort of your own home. Plus, with do-it-yourself credit improvement, all your money goes directly to the debts and you can avoid the practices that damage your credit.” In addition, see ZipDebt.com, which provides information to help consumers engage in successful do-it-yourself debt settlement (including a free, 32-page e-brochure), and says “debt settlement” is nothing more than haggling, and can be successfully accomplished by “average, everyday, ordinary people.”

Useful information and Do It Yourself assistance for solving debt problems can also be found at Nolo.com, including a calculator to determine how long it will take to pay off a particular amount of credit card debt.

The lax response of bar discipline committees to misconduct by debt-reduction lawyers in Upstate New York was, in fact, an important part of this weblog’s very first post in May 2003, and it received more detailed attention several times thereafter, including the posting “Blame bar counsel for the Andrew Capoccia Scandal” (March 8, 2005).

Note: I’ve never been a bankruptcy or debt collection lawyer, or a credit counselor, nor worked for or with one. My concern is that of a consumer and a client advocate, not a provider of a rival form of legal and credit-related services. I had originally looked into “debt negotiation” when chronic health problems forced me to close my law and mediation practice, and I accrued significant debt over the next few years of disability. Seeing their debt-reduction advertising campaign, I approached the Capoccia Law Firm, to explore ways to avoid bankruptcy (which I was able to do on my own, without using such debt-settlement services).

Let me be clear: I have absolutely no reason to think NetDebt is engaging in Capoccia-style theft and fraud. However, long before I learned that Andrew Capoccia was actually stealing his clients’ money instead of using it to pay off their debts, I worried that lawyers and others touting “debt reduction” services such as his might be using questionable tactics and charging excessive fees. A decade later, objective observers and consumer advocates continue to have similar concerns about debt negotiation services. See, e.g., “Debt Relief: Beware the Frauds” (AARP Magazine, May 2007); the Federal Trade Commission’s Debt Settlement Workshop and petition in FTC v. Edge Solutions; and “Beware Debt Elimination Scams: Costly Bogus Schemes Won’t Cancel or Reduce Credit Card Balances” by George Daleiden (Feb. 18, 2008; see Scam #2). update (Oct. 29, 2008): See our posting “FTC smites debt negotiation firms.” And (May 9, 2009): See “ATTORNEY GENERAL CUOMO ANNOUNCES NATIONWIDE INVESTIGATION INTO DEBT SETTLEMENT INDUSTRY: Subpoenas Fourteen Debt Settlement Companies and One Law Firm in Connection with Probe” (Press Release, NYS AG, May 7, 2009); and “Cuomo subpoenas debt settlement companies” (Newsday, by John Riley, May 7, 2009, which discusses the Allegro Law Firm); and Consumer Reports (March 2009), on high-fee debt settlement as a “financial trap”.

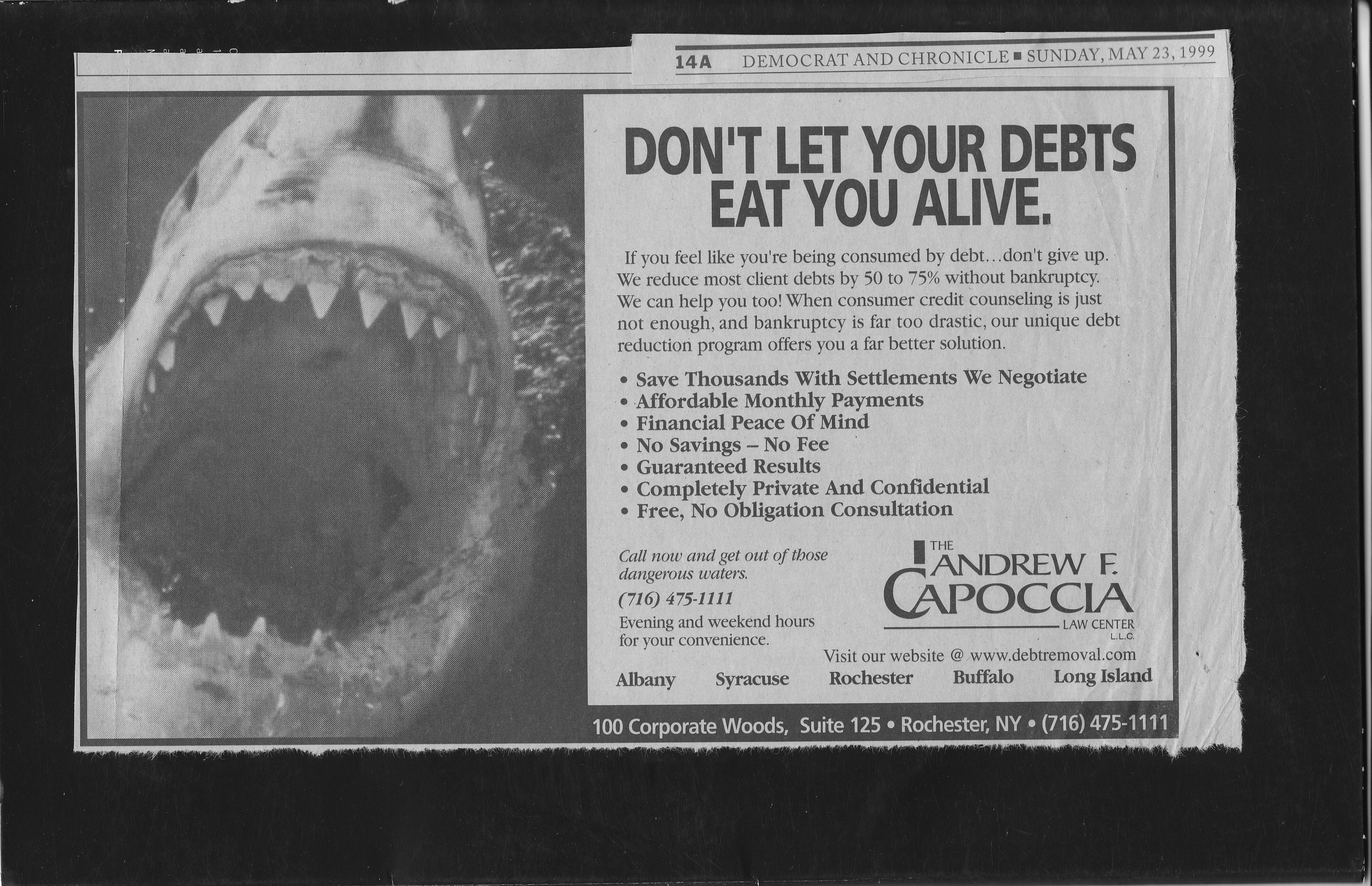

![]() Like NetDebt, Andrew Capoccia claimed to be able to reduce your debt levels dramatically, without putting you in bankruptcy. See, e.g., this 1999 ad (which ironically featured an image of a vicious shark), and this earlier TBED ad.

Like NetDebt, Andrew Capoccia claimed to be able to reduce your debt levels dramatically, without putting you in bankruptcy. See, e.g., this 1999 ad (which ironically featured an image of a vicious shark), and this earlier TBED ad.

{kind=link}

{kind=link}

Capoccia charged what he called a “small part” of the savings (25 to 27%). His massive advertising campaign was aimed at people with significant unsecured debt, who wanted to avoid bankruptcy — and who had enough money to afford his fees. Capoccia took his fees upfront, before starting “negotiation” with creditors. Negotiation amounted to sending form letters and making phone calls requesting a large reduction in the client’s debt, while withholding payments and hinting at bankruptcy to increase leverage over creditors.

Note: As one debt collection lawyer has pointed out, bankruptcy is not as threatening to creditors as it was a decade ago, due to the new creditor-friendly bankruptcy laws, which went into effect in October 2005 and which require debtors who can afford to pay off their debt to set up a plan to do so. Thus, a creditor does not usually have to worry it will be “left with nothing.” Instead, the new bankruptcy law generally means “that a debt will be extended out over a longer period of time than the creditor would normally accept with little or no interest being paid.” Despite this change, one debt settlement author insists that “The negotiation leverage is still there, because the creditor has no way to know in advance whether your case would be a Chapter 7 or a Chapter 13 bankruptcy.” As a former mediator, I think a creditor is likely to gain a pretty good idea of the debtor’s situation in any real “negotiation.” I agree, however, that the new bankruptcy laws do not remove all incentives for creditors to negotiate a reduced balance.

The Capoccia fee was a “reverse contingency fee” (based on savings achieved, rather than moneys won, for the client). His fee was taken upfront and was determined by an optimistically-forecasted percentage of debt-reduction savings, with the contingency fee set at 25 to 27% of such projected savings. He clearly wanted potential clients to conclude that the percentage was a bargain, after comparing it to the “standard” one-third (or more) taken by personal injury lawyers in Upstate New York.

The Capoccia fee was a “reverse contingency fee” (based on savings achieved, rather than moneys won, for the client). His fee was taken upfront and was determined by an optimistically-forecasted percentage of debt-reduction savings, with the contingency fee set at 25 to 27% of such projected savings. He clearly wanted potential clients to conclude that the percentage was a bargain, after comparing it to the “standard” one-third (or more) taken by personal injury lawyers in Upstate New York.

Such fees were excessive, I argued at the time (and continue to believe), because there was little risk that Capoccia would not be adequately compensated for his efforts (which involved little if any real lawyering). For example, when I met with him, he bragged — lawyer-to-lawyer, while trying to hire me, once he heard I had worked a decade for the FTC — about how easy it was to get huge reductions from creditors. By taking the fee upfront, Capoccia also removed the risk that he would not be able to collect his fee once it was actually earned. [NetDebt’s fees and related practices are discussed in detail below.]

Also like NetDebt and similar services, Capoccia had his debt reduction clients first stop making all payments to their creditors (to increase the pressure to settle for less than the full amount due), thus immediately ruining the credit status the client was trying to salvage.

Here’s how NetDebt describes its services in its FAQ::

Here’s how NetDebt describes its services in its FAQ::

“What does “debt settlement” mean? The term ‘debt settlement’ means negotiating with a creditor to reduce the amount of a delinquent debt down to a lower amount, that the debtor can then pay in order to fully satisfy (or pay off) the debt. The primary benefits of this strategy are to help you become debt free sooner, pay your debts on terms structured to your specific budget, avoid bankruptcy, and pay less than you would by making the minimum monthly payments.”

. . . “Once you enroll in the program, you will immediately stop paying your creditors, and instead start putting your monthly payments into a Trust Account that is established by the law firm. From that point on, the attorneys take over everything. Since your creditors will not be receiving monthly payments, your accounts will become past due, but in a controlled environment.”

. . . Once there is sufficient funds in your account, the lawyers will settle with the first creditor, and that process will continue until [you settle all accounts and your balance is zero].

As for their fees, NetDebt’s FAQ says:

1. What does this cost me?

+ service fees

“Although we are a free online resource and do not charge you anything for our services, the law firm does charge a retainer equal to 15% of the debts that you include in the program, plus a small monthly service fee. Please remember that all program fees are included in your monthly payment and are not due in advance. In addition, they will not start until you execute the Legal Services Agreement which will be sent to you upon completion of your online enrollment.”

[I later learned that the “small monthly fee” is $50 per month, and that you may take no more than 15 months to pay the retainer, although you can be in their program for up to 54 months; also, negotiation will not start with your creditors until you have accrued enough money in a savings account to pay off the first creditor in a lump sum.]

If you visit NetDebt’s website, you will be invited to use the NetDebt Savings Calculator to see how much money they can save you. I tried several debt amounts, and was told each time that it would cost me 12 to 13 times as much to pay off my debt on my own than if I used NetDebt. However, in tiny font at the foot of the display, I discovered that some fairly stringent and possibly unrealistic assumptions were made to show how much you’d save using NetDebt:

The total debt payment figure if you don’t use NetDebt is based on your making only the minimum monthly payment of 2% to your creditor, at the high annual interest rate of 21%. The lower-payment figure using NetDebt is based on their achieving the full 50% reduction in your overall debt, without counting accrued interest or penalties. Furthermore, while the savings comparison does count the lawyer’s fee you will pay, but does not take into account the $50 monthly service fee, the fact that interest and penalties will indeed keep accruing on your account until it is paid in full, or the likelihood that the IRS will consider any reduction in your debt to be taxable income.

NetDebt discourages the use of bankruptcy, saying it should only be used “as a LAST RESORT; pursued ONLY after all other debt relief remedies have been explored.” In FAQ #6, NetDebt tells you further that, “A bankruptcy filing is a very detrimental entry on your credit history, and can remain on your credit reports from 7 to 10 years after the bankruptcy filling has been discharged.” However:

Although FAQ #4 acknowledges, “In the short-term, your credit rating will reflect that you are not current on your debt payments which in most cases will negatively affect your credit,” it does not tell you that being past due “causes a record of late payments on your credit report that can damage your credit score for 7 years” (per TransUnion).

To learn more about NetDebt’s services and fees, I spoke with one of their service reps [“Ryan”] using their online Chat feature. I asked if I could see the Legal Services Agreement that a NetDebt client would sign with the participating law firm, but was told I could only do so “at the end of the application process. At that time you can choose to accept the agreement or decline.” (I decided not to go through a full “pretend” application process in order to see the Agreement.)

Here are excerpts of my chat with NetDebt’s service representative, Ryan:

Here are excerpts of my chat with NetDebt’s service representative, Ryan:

- Q: Do you have lawyers in every State? A: Yes. We use the Contego Law Firm. It is a network of attorneys throughout the country [Note Update: Click to see the website of the Contego Law Firm, which says it has “helped thousands” in their nationally recognized consumer protection practices, and lists two lawyers, with an office in Newport Beach, CA. Their masthead notes that contego is a Latin verb meaning “To Protect, Shield, Cover, Defend.”]

- Q: Are the legal fees due in full even if the debt is reduced by significantly less than one half?

A: I am sorry but I do not understand your question. I know that the attorneys will do everything in their power to reduce your debt. They charge a flat 15% fee for the cost of their service as well as a $50 a month maintenance fee.

. . . We can extend your program out up to 54 months if needed but the max that we could spread out the retainer fee would be 15 months.

Q: [I]f they are only able to reduce my debts by 30%, does the same flat fee apply?

A: Yes. The ultimate goal is to assist you in reducing your debts. A 30% reduction of your debts would be considered beneficial.

- Q: If a creditor refuses to negotiate and instead sues, do your lawyers handle the case as part of the fee?

A: No. Our attorneys will do everything they can to prevent that from happening. You would be refunded the money that was set aside for that particular account. [Ed. Note: not your fees]

- Q: Approximately what percent of your clients achieve a 50% reduction?

A: On average and based on our past experiences we are able to negotiate a debt to be around 45c on the dollar. Interest will continue until the account is settled. [Ed. Note: It is not clear whether this means that the average client has 45% of his or her total debt forgiven, or that the average settled account achieves a 45% reduction, while some accounts remain unsettled and their full balances plus interest and fees are still due].

The NetDebt website says, “Please remember that all program fees are included in your monthly payment and are not due in advance.” However, as you can see above, I learned during my chat session that NetDebt requires you pay the full retainer in no more than 15 months, once you sign their Legal Services Agreement. You can remain in their program up to 54 months, while paying the monthly service fee, and hopefully accruing the funds to pay off your debt. You will be paying the retainer before negotiations start with your creditors.

That means, for example, that even if you “only” have $10,000 in debt, you must give NetDebt $150 each of the first 15 months to pay both the retainer and the service fee. Any amounts paid to NetDebt over that $150 would go toward accruing a lump sum payment to a creditor. It may take quite a long time to accrue the money necessary for negotiation to start with your first creditor.

NetDebt does not negotiate a monthly payment schedule for you with your creditors based on a reduced balance due; it only negotiates lump sum settlements with your creditors. Once you enroll by signing their Legal Services Agreement, the law firms sends out a notice of representation to all of your creditors. It does not, however, start negotiating with any creditor until you have accrued enough in your savings account (after paying lawyer fees and the monthly service charge) to pay off the creditor’s debt in a full lump sum.

If one or more of your creditors has not agreed to a settlement by the end of the 54 months, the amount accrued in your savings account will be refunded to you, but not the lawyer’s fee. You will, of course, have ruined your credit rating, while accruing years’ worth of interest and penalties, and might very well have already been sued by a non-cooperating creditor and forced into bankruptcy.

According to their Chat Rep, if the NetDebt lawyers advise you to go bankrupt, and you hire them to be your bankruptcy firm, they will credit any retainer fees paid by you to their bankruptcy fee.

With this background, let’s look more closely at NetDebt’s fees, which apparently are similar to those of other debt settlement firms.

Naturally, I hope NetDebt or other debt negotiators will use our Comment box to let me know if I’ve made any factual mistakes or mis-interpretations, as well as any erroneous assumptions.

Is the total fee charged by NetDebt’s lawyers — 15% of your debt plus a $50 monthly service fee — reasonable and appropriate?

Is the total fee charged by NetDebt’s lawyers — 15% of your debt plus a $50 monthly service fee — reasonable and appropriate?

Rule 1.5: Fees of the Model Rules of Professional Conduct says “A lawyer shall not make an agreement for, charge, or collect an unreasonable fee or an unreasonable amount for expenses.” The Rule sets out the factors that go into the determination of a “reasonable” legal fee. Traditionally, the reasonableness of a fee depends primarily upon such factors as the amount of time spent performing the service; “the novelty and difficulty of the questions involved, and the skill requisite to perform the legal service properly;” the amount involved and results achieved; the experience, reputation, and ability of the lawyers performing the service; the amount of the fee in proportion to the value of the services performed; and whether the fee is fixed or contingent.

NetDebt’s Customer Service Office is located in Laguna Niguel, CA, and the Contego law Firm also has its office in California. Rule 4-200. Fees for Legal Services of the California Rules of Professional Conduct for Lawyers, enumerates similar factors for judging the “conscionability” of a fee, and adds

- “The relative sophistication of the member and the client.” and

- “The informed consent of the client to the fee.”

For an overview of my thoughts on determining the reasonableness of various kinds of fees — hourly, value-billing, and other alternatives — see “broadening the hourly-billing debate” (August 18, 2007), which includes excerpts from several other postings.

Let’s look at some of the relevant fee factors as they appear to apply to the retainer required and the legal services performed by law firms associated with NetDebt.

Let’s look at some of the relevant fee factors as they appear to apply to the retainer required and the legal services performed by law firms associated with NetDebt.

Example: According to an article in yesterday’s New York Times, half of American families have $25,000 in consumer debt. With NetDebt charging 15% of your total debt, a client who brings $25,000 of debt to the NetDebt program will pay a front-loaded, nonrefundable $3,750 in legal fees, plus an extra $50 per month service fee (which adds up to $2700, if the maximum 54 months are needed by the debtor).

If NetDebt were able to achieve a full one-half savings for such a client, $12,500, after 54 months in the program, the client would pay $6450 in fees for that savings, but the remaining balance would now have ballooned due to interest and penalties, and the IRS would consider the $12,500 savings to be taxable income. Would such a fee be reasonable, when compared to the type and amount of work performed by the lawyer and the benefits reaped by the client?

- Time Spent: It’s hard to imagine that a significant amount of lawyer time will be spent by the debt settlement lawyers. I hope they’ll let me know, if I’m wrong, but it looks to me like a very simple form letter will go out to creditors (and any active debt collectors) when the client is enrolled (basically saying “deal with us now and don’t contact our client”). Thereafter, clerical time will be used to handle the client’s monthly payments (covered amply by the monthly $50 service fee). When a large enough lump sum is banked by the client, a letter or phone call (involving no legal issues) will go to the target creditor offering to settle for a lump sum, with follow-up contacts. Since most creditors have fairly well-defined criteria for when they will or won’t reduce the client’s debt balance, the “negotiation” is unlikely to be time-consuming. NetDebt says at their website that they will “work tirelessly to settle your debt,” but the amount of lawyer time actually involved seems unlikely to be large.

- Novelty, Difficulty, Requisite Skill: Frankly, virtually no real legal issues are involved and no special lawyering skills appear needed to do “debt negotiation,” beyond insisting on the protections of the federal Fair Debt Collection Act (to prevent harassment by debt collectors) – – which are explained in this online FTC brochure, and in these tips from Nolo.com. There is no promise to litigate for the client, no body of debt settlement law to interpret and apply, no opportunity to use high-level negotiation skills. Many thousands of nonlawyers have directly and successfully asked credit card companies for debt reduction.

- As mentioned above, debt settlement Do-It–Yourself entrepreneur Charles J. Phelan describes Debt Settlement or Debt Negotiation as “good old-fashioned American haggling” and insists that “Average, everyday, ordinary people can negotiate successfully with their creditors” (especially, of course, after reading and listening to his materials). Phelan also points out that “several of the major credit card banks react to the involvement of a third-party negotiation firm with immediate legal action or hardball tactics,” making any lawyering skills or strategies irrelevant — or, counterproductive.

-

A Flat Fee: “Ryan” called NetDebt’s arrangement a flat fee, and I guess it is for each client, but it is a strange flat fee. For example:

A Flat Fee: “Ryan” called NetDebt’s arrangement a flat fee, and I guess it is for each client, but it is a strange flat fee. For example:

- There’s no distinct and measurable transaction performed by the lawyers. Typically, a lawyer charging a flat fee says, “For $X, I will complete transaction Y (e.g., a house closing, criminal defense, estate settlement, incorporation).” Instead, NetDebt is saying, “For our $XX fee, we promise to try to reduce your debts for as long as you are in our program.”

- The fee has no direct relationship to the likely amount of work to be done — not to the number of accounts or creditors to be handled by the law firm, nor to the often well-known proclivities of any particular creditor to engage in “negotiation” with a third party or the debtor. A client could have a large amount of unsecured debt held by only one or two creditors, or owe money to many different creditors. Some of those creditors might be negotiation-friendly, while others might be known to refuse to deal with any third-party.

Aside re Certainty: Advocates of flat fee arrangements often point to the benefits for the client from having certainty as to the overall cost. That is, of course, particularly true when estimating the hours of work needed to complete the task is nearly impossible at the outset, due to unknown factors, and the range of possible outcomes is great. (From my own practice, I’d say that a divorce with children and an antitrust merger investigation are two kinds of cases where it can be very difficult to quantify an hourly fee in advance.) However, as we said here in January 2004, justifying a percentage fee or a flat fee by saying “but, the client has certainty” is often a rationalization for a fee that is simply too large for the amount and type of work actually done by the lawyer and the benefit conferred on the client.

I continue to agree with the Illinois State Bar Association’s brochure on Fee Disputes Between Lawyers and Clients, concerning the basis of a reasonable fee (which is no longer online; the emphasis is added):

“Abraham Lincoln, himself a lawyer, once said, ‘A lawyer’s time and advice are his stock in trade.’ The basic ingredient is the amount of time spent.”

Similarly, courts in Michigan, when discussing the reasonableness of the percentage fee charged by the estate representative in probate, have stated that the statue authorizing “reasonable compensation for services performed . . . implies that the amount of work performed and the benefit conferred on the estate are important factors in calculating a fiduciary fee.” (emphasis added.)

- A Percentage Fee: How can we judge the reasonableness of the percentage fees charged by NetDebt and other debt settlement firms, other than looking at the likely amount of work to be done and the benefits achieved for the client? I’m sure that many of the firms are hoping the over-extended and distraught client will favorably compare a 15% fee to the percentage fee best known by the average consumer: the one-third or 40% standard contingency fee charged by personal injury lawyers. Of course, people in the legal profession know that such a comparison is very tricky.

Not a Contingency Fee. As explained in our series on the ethics of contingency fees, they are justified by the amount of risk taken by the lawyer of doing a significant amount of work without being adequately compensated [with 33.3 or 40% being the maximum amount allowed in most jurisdictions]. I argued a decade ago that Andrew Capoccia’s contingency fee of 27% of the achieved debt reduction was excessive, because he was assuming a tiny risk of expending significant amounts of unpaid attorney time, or other resources, for his debt reduction clients (and, because he took the fee upfront, negating worry about collecting the reverse contingency fee from the client). Even if we do not count that $50 monthly service charge, a fee of 15% of total debt is even less justified than Capoccia’s 27%, because:

- There is no contingency here — it is a flat retainer fee, paid regardless of results.

- 15% of total debt amounts to 30% of the savings, if NetDebt actually achieves the one-half reduction that is the best result promised to its clients. Should they only achieve a 40% overall deduction for the client, the 15% fee would amount to over 37% of the savings achieved.

Front-loaded, too. The debt settlement industry has, therefore, increased its fees in switching away from contingency fees to the flat percentage fee. As the ZipDebt Blog explains in the posting, “Debt Settlement Front-Loaded Fees Not in Consumers’ Best Interests” (April 3, 2006), front-loading the fees (taking them in the first 6 to 15 months) further hurts the client because it takes so long to accumulate a big enough lump sum to offer for settlement to any creditor. Besides decrying the “sheer size” of the fees, and noting that the delay results in a significant amount of added interest and penalties for the credit card holder, ZipDebt’s Charles J. Phelan says:

“The big problem here is that some of the best deals happen right before chargeoff, which is usually in the 6th or 7th month of the program. So this means that some of the best deals cannot be taken, because too much money has gone to fees and not enough toward savings for settlements. In the old day, the fees were on the back end, charged only after successful settlement.”

Compared to Other Percentage Fees: Keeping in mind the kind of services provided by debt settlement lawyers such as NetDebt, we might want to look at other situations where lawyers charge a percentage fee for legal services. Attorney’s fees in probate court are usually a statutorily prescribed fixed percentage of the probate estate. “This percentage fee applied to the probate estate can be as little as 2.5% in North Carolina or Virginia and as much as 6% in New York or Pennsylvania.” (The CPA Journal) In California, for example, the statutory rates under the Probate Code for smaller estates are:

4% on the first $15,000. [$600]

3% on the next $85,000. [$2,550]The percentage declines for larger estates. According to one California probate and estates lawyer, however, they “are not mandatory fees, and most attorneys will negotiate a lower fee.” These numbers, for performing defined tasks (some of which actually entail applying legal knowledge) are quite a bit smaller than NetDebt’s 15% fee for its unspecified service and iffy results.

![]() It’s time to wind up this lengthy posting. I’ve gone into a lot of detail, because a legal fee needs to be looked at in its context when determining its reasonableness. Of course, I can’t make this into a heavily-researched monograph or law review article on ethical lawyer fees. My hope is that readers — especially, but not limited to, legal professionals — will offer their thoughts on whether the legal fee structure outlined above for debt negotiation services is excessive (without vulgarities or personal attacks, please). [Note: There may be a delay between your leaving a Comment and my “moderating” it to allow it to appear online, as I cannot be at my computer 24/7.]

It’s time to wind up this lengthy posting. I’ve gone into a lot of detail, because a legal fee needs to be looked at in its context when determining its reasonableness. Of course, I can’t make this into a heavily-researched monograph or law review article on ethical lawyer fees. My hope is that readers — especially, but not limited to, legal professionals — will offer their thoughts on whether the legal fee structure outlined above for debt negotiation services is excessive (without vulgarities or personal attacks, please). [Note: There may be a delay between your leaving a Comment and my “moderating” it to allow it to appear online, as I cannot be at my computer 24/7.]

I know lawyers are reluctant to discuss fees in public, and especially to decry excessive fees, but we owe it to our clients and the profession to think about and debate these issues — and not merely act as if all alternatives to hourly billing are fair and ethical in every circumstance. [My post on “broadening the hourly-billing debate” compiles a lot of my thinking on the matter.]

A number of lawyers with weblogs have discussed the use of flat fees and value billing in their practices, and I hope they will join in the conversation. For example, New York Divorce lawyer, Daniel Clement, and Indiana family law practitioner Sam Hasler; and the always-modest “Greatest American Lawyer.”

In general, the bar — a self-regulating profession with little outside oversight — has done a rather poor job enforcing its ban on unreasonable fees. At times it seems that only actual cases of theft, fraud or clearcut billing abuses are prosecuted by bar counsel (e.g., bill padding, or gigantic self-generated bonuses). Likewise, the judiciary seems to enter the fray only if mandated by a particular statute (such as probate or class action laws) or when confronted by a scandalously large fee in a tort case. Therefore, in addition to more diligent watchdogs, our clients deserve a broader discussion of what constitutes a reasonable fee. That is especially true when it comes to “alternatives” to hourly billing, which have been much championed, but not much analyzed from the ethics perspective.

In closing, here is one formulation that I offered a couple years ago in the context of percentage billing:

A good rule of thumb for a fiduciary (or any service-provider): If you’re embarrassed to tell your client/customer how little you have to do to accomplish the task, when compared to the fee, your fee is too high. That’s why many informed consumers have rebelled against the customary real estate agent percentage when selling a home (which tends to be in the 6 to 8% range, depending on your locality). It’s also why a lot of probate courts have questioned or put a dollar limit on probate fees based on the overall value of the estate.

At a minimum, when the lawyer is using a fee significantly greater than what a reasonable hourly rate would produce, the lawyer needs to make sure that the client fully understands the situation — including just what you will be doing for him or her. The requirement of Model Rule 1.4 (b) that “A lawyer shall explain a matter to the extent reasonably necessary to permit the client to make informed decisions regarding the representation,” applies to setting fees as much as it does to litigation strategy, and particularly applies when the client is an unsophisticated buyer of legal services.

As I have said numerous times at this website: Alternatives to the hourly fee can indeed be ethical and should be encouraged — because they are a spur to creating the efficiency, innovation, and competition that lead to better client service and lower fees, not in order to lull the client into paying higher fees.

update (July 25, 2008): In response to this posting, debt settlement expert Charles Phelan has written an extensive “History of Debt Settlement Fees” at The ZipDebt Blog (July 25, 2008), which adds important insight and perspective for assessing the industry’s fees. Charles estimates that “about 99% of settlement companies charge fees based on the front-loaded model” with a flat 15% of total debt as the new industry standard, plus large monthly service fees. He adds that “the magic 15% flat fee . . . has no bearing whatsoever on the amount of actual work involved in negotiating debts.” Charles concludes:

“In my estimation, this front-loading of the program fee removed the single most valuable aspect of the program from the consumer’s perspective – namely, that the fees were based on results achieved. . . . This, of course, was wonderful for the debt settlement company, but a horrendously bad deal for the customer. In effect, the settlement company had now become just another creditor, elbowing out of the way the client’s legitimate creditors, and grabbing up front most of the money that should properly have gone toward settlements.”

In a lengthy Comment to this posting, Charles has also given his insights on many other aspects of debt settlement.

p.s. (July 23, 2008): While looking for a quote on a different topic this afternoon, I was leafing through one of my favorite books about the legal profession, The Betrayed Profession (1999), by Sol Linowitz. By chance, I came across the following passage (also found in the June 1999 issue of DCBA Brief), which makes a nice postscript to the above posting:

“As recently as 1963, Everett Hughes wrote that the central feature of professionalism was a doctrine of credat emptor –“let the buyer trust” — rather than the commercial maxim of caveat emptor — “let the buyer beware.” Society counts on the law, and on lawyers as its servants, to spread such feelings of trust through the community. Instead, too often, we help weaken them.”

Speaking of trust, Blawg Review‘s Ed Post reviews the book The Trusted Advisor today, strongly recommending it for young lawyers.

update (Oct. 29, 2008): A Wall Street Journal column “Debt-Releif Firms Attract Complaints” says there’s been a large increase in complaints about the so-called debt-negotiators, and “Regulators, consumer advocates and industry groups are taking a closer look at debt-settlement firms.” (by Eleanor Laise, Oct. 14, 2008). At the WLJ site, you’ll find links to related podcasts, too: John Ulzheimer, president of consumer education for Credit.com, talks with Eleanor Laise about the growth in debt settlement companies and whether they deliver on their promises.

afterwords (July 22, 2008): Many thanks to Scott Greenfield at Simple Justice for his lengthy piece responding to this posting, “Are lawyers stealing from the (not so) poor?” (July 22, 2008). Scott concludes:

“While this niche practice will no doubt bring a handful of lawyers a lot of money in this recession difficult economic time, it feeds into the public’s disgust for the profession. And with good reason. “

(July 22, 2008): And, with gratitude, to the very generous Holden Oliver, at What About Clients?: you are very welcome.

(July 24, 2008): Thanks to Public Citizen lawyer Greg Beck for posting on this topic, and pointing to our posting at the Consumer Law & Policy weblog. See “Questionable ‘Services’ of Debt Settlement Firms” (July 24, 2008)

(July 28, 2008): Welcome to the many readers of Overlawyered.com who saw Walter Olson’s kind pointer to this posting this morning and stopped by to take a look.

(July 29, 2008): Hello and thanks to Philadelphia lawyer Maxwell Kennerly, for his post “The Wrongfulness of Debt Negotiation Fees” (Litigation and Trial weblog, July 29, 2008).

Here because this was so highly touted by What About Clients? Was just going to skim, but couldn’t stop reading. What a great post. Nice to know there are lawyers like you out there countering lawyers like this.

Comment by Dan — July 24, 2008 @ 10:06 am

Many thanks, Dan, for your kind reaction and remarks. I hope other blawgers will help spread the word, and that bar counsel across the nation decide to investigate.

Comment by David Giacalone — July 24, 2008 @ 10:18 am

[…] attorney and longtime consumer advocate David Giacalone has written an excellent piece on the subject of debt negotiation fees. Although I’m sure his post will not win him many fans in the settlement industry, I for one […]

Pingback by The ZipDebt Blog»Blog Archive » The History of Debt Settlement Fees — July 25, 2008 @ 6:34 pm

David, many thanks for a truly insightful piece. As the author of The ZipDebt Blog cited in your post, it was especially rewarding to see confirmation from a member of the legal profession that the 15% front-loaded fee structure is simply inappropriate and unjustified. I’ve just posted an article on my blog that discusses the history of how the 15% fee structure evolved in the first place, and some of your readers may find that additional information to be enlightening.

I’d also like to touch on a few points raised in your post.

1. You write, “Also like NetDebt and similar services, Capoccia had his debt reduction clients first stop making all payments to their creditors (to increase the pressure to settle for less than the full amount due), thus immediately ruining the credit status the client was trying to salvage.”

The simple fact is that banks will only settle for significant discounts as a loss-reduction procedure. An account that is approaching 180 days delinquency is fast becoming a candidate for “charge-off,” where the creditor takes a 100% loss on their books and then attempts to recover through the collection process. Settlement, in effect, becomes a “write-down” rather than a full write-off of the balance. So it’s usually not possible to obtain a reasonable settlement until that deadline looms. As to the point about credit damage, consumers considering debt settlement should clearly understand that it provides an alternative to a five-year Chapter 13 bankruptcy. Anyone “trying to salvage” their credit status simply has no business being in a debt settlement program in the first place! I realize that this may not square with how settlement programs are presented to the consumer, but simply put, debt settlement and bankruptcy are roughly equivalent in damage to credit. Therefore, settlement only makes sense if the client is already headed for a credit meltdown anyway.

2. Regarding the issue of taxes owed on forgiven balances, it is true that consumers will receive 1099-C forms from the creditor for any canceled balance of $600 or greater. However, there is a provision known as the “insolvency rule,” whereby a debtor is permitted to exclude the 1099-C figure from ordinary income up to the amount by which they were insolvent at the time of settlement. Many, if not most, debt settlement clients have a negative net worth and therefore meet the insolvency definition. So the exposure on tax liability is not quite as bad as some industry critics claim.

3. I found the online chat exchange with the company’s sales rep to be quite interesting. You asked, “If a creditor refuses to negotiate and instead sues, do your lawyers handle the case as part of the fee?” The rep replied with, “No. Our attorneys will do everything they can to prevent that from happening. You would be refunded the money that was set aside for that particular account.”

This is interesting, because I’m not aware of any settlement company that establishes separately funded accounts for each individual debt. In other words, funds are pooled into a single escrow account. So there is no way to determine whether or not funds were set aside for any particular account.

4. You indicated that the service agreement includes language that the law firm sends out notices of representation to all of the client’s creditors. This, quite simply, is like waving a bright red flag in front of a charging bull! Whether or not the settlement firm is also a law firm, the major creditors simply do not recognize third-party debt settlement as a legitimate business model. Nowadays, early notification to original creditors is a fast track to escalated collection attack, arbitration filings, and lawsuits. So not only does the client have to pay 15% up front, they are making matters MUCH worse on themselves in the process.

5. Regarding the attorney model for debt settlement, the theory is that the client will have an attorney to turn to in their home state if they do get sued by a creditor. This, in my opinion, is nothing more than a “fig leaf” designed to give the consumer the illusion of security. Many firms do not actually have attorneys in all of the states in which they accept clients. And even if they do, that security is an illusion, simply because the service agreements typically contain clauses that clearly state the firm does not provide representation in legal matters. At most, an attorney might assist the debtor in preparing an answer to a lawsuit, merely for the purpose of postponing a judgment and stalling for time to raise funds. But the normal outcome of such a negotiation is either a high-percentage settlement (70-85%), or a stipulation for judgment with the full balance to be repaid over some period of years at the nominal judgment rate of interest for that state.

6. Some of the agreement language you cited discusses program duration in terms of 54 months. A 54-month debt settlement program is totally absurd! It will require another blog post to describe the evolution debt settlement program duration, but the original idea was 36 months max. Even that duration is no longer practical, due to the greatly increased incidence of litigation by the secondary debt purchasing industry. Today, a consumer should aim to settle the accounts in 12-18 months to keep the risk of litigation within manageable limits. If the client’s resources are so thin that they will need 54 months to get everything settled, then Chapter 13 bankruptcy is likely to be a better option (assuming they do not qualify for Chapter 7).

Comment by Charles Phelan — July 25, 2008 @ 6:44 pm

Charles, Many thanks for sharing your experience and perspectives on many aspects of Debt Settlement.

I urge readers to also read your new posting at The ZipDebt Blog, “The History of Debt Settlement Fees” (July 25, 2008). I’ve discussed it in a new Update in the body of this post, but the entire posting is worth a read by anyone who wants to understand this industry and its fee structure.

Comment by David Giacalone — July 25, 2008 @ 10:50 pm

Another thing these debt negotiation operations don’t tell you is that the IRS considers forgiven debt to be “taxable income.” So, you get 40K of that debt written off, you just realized 40K of taxable income.

Bankruptcy is exempt. Forgiven debt is not “income” if it was forgiven in bankruptcy. But otherwise, debt forgiveness, short sale of a home, deed in lieu of foreclosure… doesn’t matter. It’s taxable income.

Comment by Seth R. — July 26, 2008 @ 6:01 pm

[…] what strapped consumers are getting in exchange for the high fees many such attorneys charge (Jul. 21; see also Greenfield, Jul. 22, and ZipDebt, Jul. 25, via, Greenfield again, Blawg Review […]

Pingback by Overlawyered.com — July 28, 2008 @ 8:32 am

I’m so glad I found this before my website becomes full-blown for now I am in a better position to give advice to these vulnerable people. Thank you so much for this valuable information which will be of so much help to all concerned. You can be sure I will keep following up this site so I can keep abreast of the latest changes.

Evelyn

Comment by Evelyn — July 28, 2008 @ 4:18 pm

[…] doubts over debt negotiation fees | f/k/a (via Consumer Law & Policy) […]

[Ed. Note: See Caveat Emptor weblog, “Debt Settlement companies . . are they worth the fee?” (July 30, 2008)]

Pingback by Sam Glover — July 30, 2008 @ 7:52 am

I wish I had found this website a few months ago, I am one of the people that have been sucked into the underworld of debt settlement by “NetDebt” and the Contego Law firm.

I was getting behind in my credit card bills and was becoming desperate for some kind of help. I filled out the online form and felt a sigh of relief because, guess what, I did not have to talk with anyone in person. I was and continue to be ashamed of the situation that I have gotten myself into. I am now facing a lawsuit that “is usually a last resort” according to the Contego Law Packet that I received. I contacted them and they sent me a letter to forward to the courts about how they were not representing me but offer to have a structured settlement at the 50% Industry Standard. I really do not know what to do at this point. I am paying in 375.00 per month to settle as quickly as possible. I am embarrassed to even be in this situation but here I am. Any suggestions anyone?

Thanks for the blog

Comment by Tim — November 22, 2008 @ 9:24 am

Tim,

Your situation is NOTHING TO BE ASHAMED OF.

Debt settlement DOES WORK. However, the settlement firm must have your best interest in mind. taking fees upfront does not help your situation.

I own a debt settlement firm and will give you all the FREE ADVICE you want….

Pretty easy math given the situation. If your plan calls for 50% offers and it takes 3 years to save for this…..

how much faster would you be done if ALL YOUR MONEY were going to the debts?

We are a service fee based firm. We only get paid AFTER your debts are settled…

I do not want to get in the middle of your current agreement with these folks, but will be willing to talk to you and give you the ENTIRE TRUTH ABOUT THIS INDUSTRY.

800-DEBT-303

Or do a Google search for my name

“TOM BATES DEBT”

Comment by Tom — December 10, 2008 @ 3:31 am

Tom, I was a little reluctant to leave all of your Comment-Advertisement up, but I thought it was an interesting and revealing.

What kind of Free Advice are you offering Tom? Tips on how to do the negotiating himself? On getting his upfront fees back?

I went to your website and could not find a word about how much you actually charge. To be honest, that always makes me a bit suspicious — especially for a service that traditionally has always seemed over-priced. I’m also curious about just how your fees are paid — what money pot does it come out of?

Comment by David Giacalone — December 10, 2008 @ 9:41 am

Hi Tim

Just curious. I am currently in the process with Debt.com – it seems they use contego law also- I am now hestitant. For what reason are you being sued? They stated that rarely ever happens, but that was a big concern I had..Please let me also know how your over feeling

Comment by bill — December 17, 2008 @ 9:30 am

David,

Thanks for sharing this. I have been a victim of a scam by a debt settlement company a couple years back. There are many companies out there waiting to gulp down the hard earned money of debt burdened individuals.

I was not aware of my rights until one of my friends referred me to debtconsolidationcare.com The members there helped me to learn many things about debts.

David, I thank you once again for your efforts in keeping the scams at bay and for keeping the common people informed.

God bless you.

Comment by Sammy — January 13, 2009 @ 12:45 am

I am currently a representative for a marketing firm (similar to NetDebt) that also refers clients to the Contego Law Firm. All allegations that have been made by your post are undeniably true, and I question our business practices every day I go to work. After reading your post it angers me to realize how much money is placed in Contego’s coffers while so little work is actually being done, and how underpaid I am while I do the majority of the work. Please let me know if there is anything I can do as an insider to help you better inform your readers.

Comment by Chris — January 28, 2009 @ 2:31 am

Thank you for writing, Chris, and for the offer of information. Most prospective customers would probably want to know what percentage of clients have truly “successful” outcomes (with most of their debt forgiven), what factors are most likely to result in such success, and how long the process takes. Also, please help us understand better what “negotiation” entails — what do these guys do that the typical customer could not do for himself or herself?

Comment by David Giacalone — January 28, 2009 @ 8:52 am

I worked with Debt.com and Contego law in a capacity I can not share for legal purposes. They are both affiliated with Interservice Financial Solutions, a company out of Maryland. I could go on and on about the unscrupulous practices of debt companies but that has been addressed many times over. Specifically, in this case, James R. Dougal, who is listed on the Contego Law Website as one of two individuals employed by Contego Law, is actually not a licensed attorney. He runs the law firm and borrows the law license of Jason Cruz, but has never been admitted to any bar. . . .

Comment by Dan — February 25, 2009 @ 6:06 pm

Thank you for your comment, “Dan.” I removed the last portion, because I have no way to verify the facts and this is the last day this weblog will be adding new content (it will remain online).

I checked today and see that Mr. Dougal is not a member of the California Bar. Their website is artfully worded (big surprise) to blur the issue, while touting his law firm experience elsewhere. Mr. Cruz, in the other hand, is shown on the Contego site to be a Member of the California Bar. Since I do not know what duties Mr. Dougal performs for the Contego Firm, I have no idea whether he is holding himself out to be a member of the Bar. Please consider bringing this matter up with the State Bar authorities.

Comment by David Giacalone — February 28, 2009 @ 2:26 pm